2026 is changing the way accounting works. The old days of hours spent on numbers and spreadsheets are ending. Today, new accounting trends are making work faster, smarter, and more profitable. From cloud accounting trends to new income tax accounting trends and powerful AI tools, businesses are finding better ways to manage money.

These financial and Accounting trends are not mere ideas; they assist firms to save time, minimize errors, and increase profits. In this blog, we explain the top 7 accounting trends in 2026 so you can understand what matters most for your business.

Table of Contents

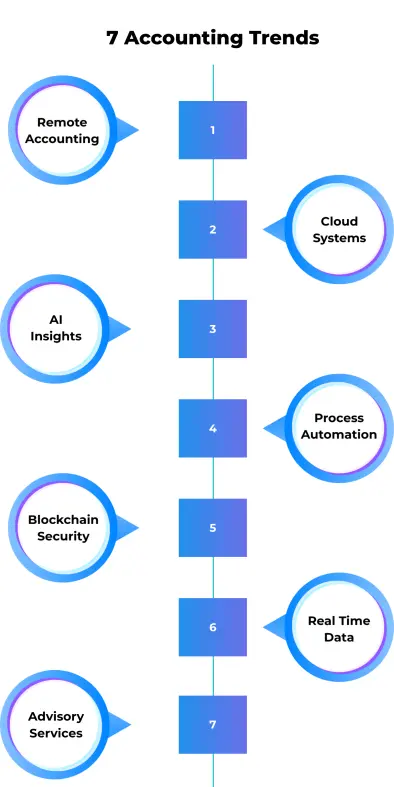

The Best 7 Accounting Trends in 2026

Accounting is no longer just about managing numbers. In 2026, accounting trends are focused on helping businesses grow faster, reduce costs, and make smarter decisions. From automation to cloud systems, these financial and accounting trends are reshaping how firms operate.

Let’s explore the latest accounting trends that are directly driving profits.

1. Remote Work is Reshaping Modern Accounting

Remote work is transforming how accounting firms operate in 2026. It is no longer just an option but a standard practice, supported by digital tools and cloud-based systems. This shift allows accounting teams to collaborate in real time, no matter where they are located.

As part of the evolving accounting trends, remote work is helping firms become more agile and scalable. Businesses can now build flexible teams, improve workflow efficiency, and maintain continuous operations without being tied to a physical office.

How it boosts profits:

- Increases productivity through flexible work environments and better time management

- Enables access to a wider talent pool, helping firms hire skilled professionals and improve service quality

- Supports business scalability, allowing firms to grow without increasing overhead costs

2. Cloud Accounting Trends Driving Business Growth

Cloud accounting trends continue to dominate in 2026. Businesses are moving their financial data to secure cloud platforms where everything is accessible in real time.

This makes it easier to manage accounts, collaborate with teams, and integrate tools like payroll and CRM systems.

How it boosts profits:

- Reduces IT and maintenance costs

- Provides real-time financial visibility

- Improves speed and accuracy of reporting

3. AI is Transforming the Future of Accounting

Artificial Intelligence is one of the most powerful latest accounting trends. AI tools can analyze large amounts of data, automate reports, and even predict financial outcomes.

With AI, accountants can move beyond routine number-crunching and focus on strategic planning and advisory services. This technology helps firms identify opportunities for growth, uncover potential risks, and make informed decisions faster than ever before.

How it boosts profits:

- Reduces financial losses by identifying risks, anomalies, and inefficiencies before they grow

- Increases revenue opportunities by identifying high-performing clients, services, and cost-saving areas

- Improves decision speed, allowing businesses to act on profitable opportunities before competitors

4. Automation is Eliminating Repetitive Tasks

Automation is changing how daily accounting tasks are handled. From invoicing to bank reconciliation, everything can now be done faster with minimal manual effort.

This is one of the most practical financial and accounting trends because it directly improves efficiency.

How it boosts profits:

- Speeds up financial processes, allowing businesses to complete more work in less time

- Reduces errors in invoices, payments, and reports, preventing financial losses

- Improves overall productivity, enabling teams to handle more clients and increase revenue

5. Blockchain is Building Trust and Transparency

Blockchain technology is slowly becoming part of modern accounting trends. It creates secure and tamper-proof financial records, making transactions more transparent.

This is especially useful for audits and compliance processes.

How it boosts profits:

- Reduces financial losses by preventing fraud and data manipulation

- Saves time in record checking, so work gets done faster

- Builds trust with clients faster, which helps close deals quickly and grow business

6. Real-Time Data is Powering Faster Decisions

One of the most impactful latest accounting trends is real-time financial reporting. Businesses no longer need to wait for monthly reports.

They can now track business performance, expenses, and cash flow instantly. This allows faster and more informed decisions.

How it boosts profits:

- Helps identify losses and financial gaps early, reducing unnecessary cost

- Improves cash flow control, ensuring better use of available funds

- Enables faster decision-making, helping businesses respond quickly to opportunities and increase revenue

7. Advisory Services are Becoming a New Revenue Stream

Accounting firms are moving beyond bookkeeping. Offering advisory services is one of the fastest-growing financial and accounting trends in 2026.

Accountants now help businesses with budgeting, forecasting, and growth strategies. This adds more value and opens new income opportunities.

How it boosts profits:

- Creates additional revenue streams

- Provide industry-specific advisory packages tailored to niche markets to grow client portfolios

- Help clients improve profitability, justifying higher service pricing while increasing your margins

Suggested: The Importance of Real-Time Data Reporting in Modern Business

Stay Ahead With These Accounting Trends

The world of accounting is changing fast. The top accounting trends in 2026, from AI and cloud accounting to advisory services and tax automation are all shaping a smarter, faster, and more profitable future.

Embracing these financial and Accounting trends will assist firms to save time, minimize errors, protects data, and provide more valuable services. Whether you are an accountant, business owner, or finance leader, understanding and using these trends will give you a real advantage in 2026 and beyond.

Frequently Ask Questions

What is accounting for income taxes?

Accounting for income taxes is the process of recording and reporting the amount of tax a business owes to the government in its financial statements. It ensures that tax expenses are properly calculated and shown in the correct accounting period. It mainly follows the matching principle, meaning tax expense is recorded in the same period as the income it relates to.

What is the Big 4 in accounting?

The Big 4 in accounting are the four largest accounting firms in the world. They are Deloitte, PwC, EY, and KPMG.

0 Comments