Accounting automation has emerged to be one of the most effective way in enhancing accuracy and reinforcing financial operations in the world of modern business. Consider having a world where manual processes such as data entry, bank reconciliation, and payroll processing occur effortlessly without errors, fatigue, and delays. That is no longer a figment of imagination, but it is a reality today with accounting automation tools which significantly minimize errors, enhance speed, and add value to financial teams.

This blog will discuss how automation is changing the accounting environment, why business of all sizes depend on it and how it removes expensive errors, which used to haunt accounting departments throughout the world. From basic bookkeeping to complex payroll management, accounting automation is the key to accuracy, compliance, and smarter decision‑making.

Table of Contents

Why Manual Accounting Causes Errors

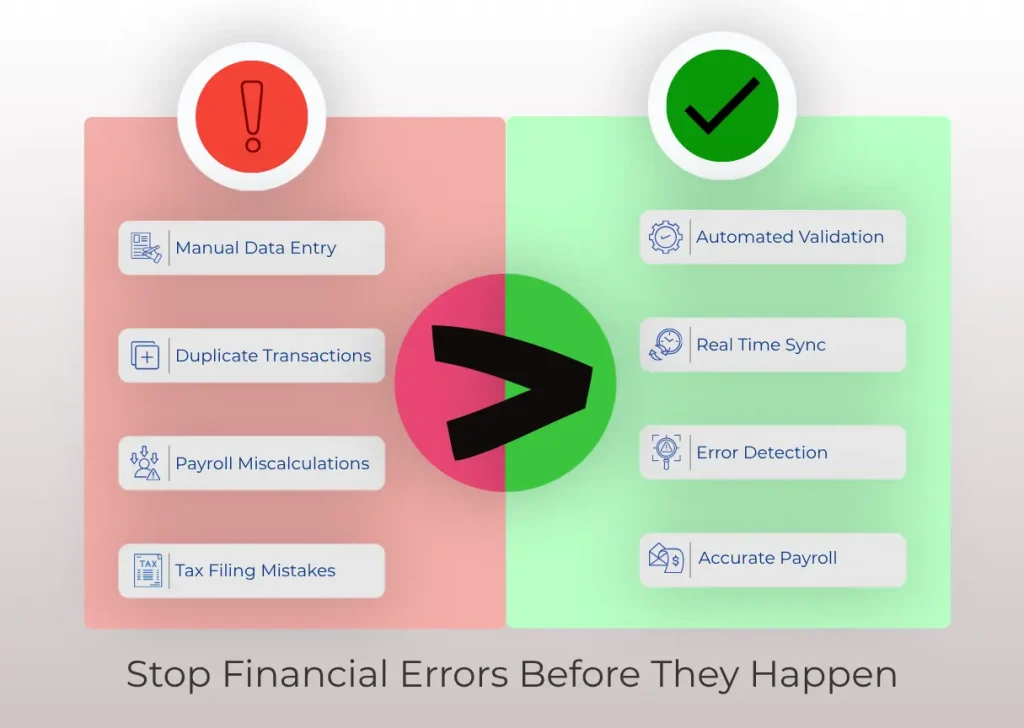

Accounting work has traditionally involved heavy amounts of manual effort — typing numbers into spreadsheets, copying figures between reports, reconciling bank statements, and calculating payroll. These are tasks that are prone to human error and they include:

- Incorrect data entry – typos or misplaced digits.

- Repeated or lost transactions – resulting in incorrect balances.

- Wrong classification of accounts – this leads to incorrect financial statements.

- Manual calculations for taxes and payroll – can lead to wrong payments, missed deductions, and compliance penalties.

Even the most experienced accountants are prone to error, primarily when dealing with large amounts of data under tight deadlines. These errors may cause financial mistakes, non-compliance with the tax authorities, bad decisions, loss of stakeholder trust, and even expensive fines.

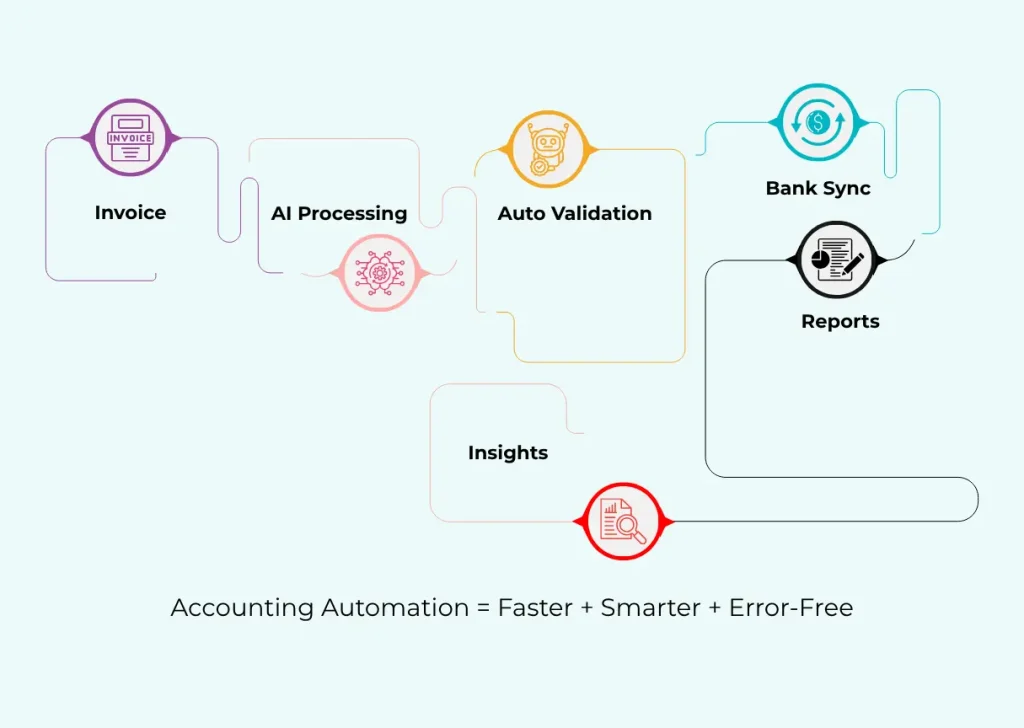

6 Ways Accounting Automation Reduces Financial Errors

Accounting automation helps businesses avoid costly mistakes by handling key tasks accurately and quickly. Here are six ways it reduces financial errors:

1. Eliminates Manual Data Entry Mistakes

One of the largest sources of accounting errors is manual data input. Automation tools like QuickBooks, CapiPlan automatically receive data on invoices, receipts, bank feeds, and other data and then key them directly into the accounting system. This eradicates any mistakes in typing, missing numbers, or entries. Many solutions also include auto‑validation features that check for discrepancies before saving entries.

2. Prevents Data Mismatches with Real-Time Integration

With automation, data flows seamlessly between different systems. For example, from sales platforms to accounting software, and from payroll systems to financial reports. This end‑to‑end integration minimizes manual transfers which tend to disrupt or misalign information.

This not only enhances accuracy but also makes financial records up to date and provides a business with a good and accurate real time picture of their finances.

3. Reduces Compliance and Tax Calculation Errors

Modern accounting automation solutions also have built-in compliance functionality that automatically updates the most current tax provisions, statutory requirements, and accounting standards. This helps companies avoid penalties from filing late or incorrect tax documents. In the case of payroll, automation updates statutory deduction rules for taxes and benefits, delivering accurate calculations every time.

4. Detects Bank Discrepancies Instantly

Reconciling bank statements manually can be tedious and error‑prone. Automated accounting systems compare transactions with bank balances, identify discrepancies and show records that are not matched, to review all in a fraction of the time it would take manually.

5. Minimizes Payroll Calculation Errors

One of the trickiest areas of accounting is payroll, where small errors can lead to dissatisfied employees. Payroll accounting automation minimizes this risk by performing calculations of salaries, tax withholdings and statutory deductions according to pre-defined rules. This minimizes mistakes that once resulted from spreadsheet errors or manual calculations.

6. Ensures Accurate and Error-Free Financial Reports

Creating financial reports manually may require days and often involves copying and pasting data across various documents. Accounting automation tools generate reports instantly, complete with graphs, dashboards, and real‑time figures. This not only saves time but lowers the risk of formatting and calculation mistakes.

Suggested: AI in Accounting: Why Every Startup Needs It Today

Top Benefits of Reducing Accounting Errors with Automation

Here are the key benefits of automation reducing accounting errors:

1. Improved Accuracy: Automation removes manual data entry mistakes like typos, duplicate entries, and wrong calculations. This keeps financial records more accurate.

2. Faster Financial Processes: When errors are reduced, there is less time spent fixing mistakes. Reports, reconciliations, and approvals happen much faster.

3. Lower Risk of Financial Loss: Small accounting errors can lead to penalties, overpayments, or missed invoices. Automation helps prevent costly mistakes.

4. Better Compliance: Automated systems follow built-in rules and tax regulations. This reduces the risk of non-compliance and audit issues.

5. Real-Time Error Detection: Automation flags unusual transactions or mismatched entries instantly. Problems are fixed early before they grow bigger.

6. Stronger Audit Trail: Every transaction is recorded with proper tracking. This makes audits smoother and improves transparency.

7. Increased Productivity: Accountants spend less time correcting errors and more time on financial planning and business growth.

8. More Reliable Financial Reports: When errors decrease, financial reports become more trustworthy. This helps business owners make better decisions.

Choosing the Right Accounting Automation Solutions

If your business is ready to adopt automation, consider the following:

- Compatibility with current systems: Choose tools that work easily with your existing accounting, banking, and sales systems. This helps information move smoothly between systems and reduces manual work.

- Error‑detection and alerting features: Good automation tools can spot unusual transactions or mistakes. They send alerts so businesses can fix problems early before they become bigger issues.

- Real‑time dashboards and reporting features: Automation tools should provide live dashboards and instant reports. This helps business owners quickly see their financial performance and make better decisions.

- Payroll features: Look for tools that support payroll accounting automation. These systems calculate salaries, taxes, and deductions automatically and help ensure payroll follows regulations.

- Cloud‑based solutions: Cloud-based accounting tools store financial data online. This allows users to access information anytime, keeps data secure, and ensures records are safely backed up.

Whether you choose a full enterprise platform or a specialized tool for tasks like invoicing and reconciliation, the best accounting automation solutions will future‑proof your financial operations.

Conclusion: Future‑Ready Finance Starts with Automation

The accounting revolution has seen the development of manual bookkeeping systems using a piece of paper to computerized intelligent systems that have revolutionized how businesses handle their financial records. The long hours of entering data manually and correcting errors are gone, the current best accounting automation applications can process repetitive jobs with accuracy, minimize expensive errors, and allow accountants to dedicate time to value-added work that leads to growth.

From real‑time accuracy to compliance confidence and greater strategic insight, automation cuts both risk and workload, making accounting smoother, smarter, and far more reliable. Whether you’re a startup, a mid‑sized company, or an enterprise in UAE accounting automation services or global markets, embracing automation isn’t just a trend – it’s a strategic move toward a more accurate and more efficient financial future.

Start integrating accounting automation solutions today and let technology handle the numbers – so your business can handle success.

Frequently Ask Questions

What is the best accounting automation tool?

The best accounting automation tools depend on business size and needs, but some of the most widely used and highly recommended tools include CapiPlan, QuickBooks Online, Xero, or FreshBooks.

What are the 4 pillars of automation?

The four pillars of automation are resilient, intuitive, secure, and end-to-end. Resilient means the system can handle errors and continue working smoothly. Intuitive refers to easy-to-use automation systems, while secure ensures data and processes are protected. End-to-end means automation covers the entire process from start to finish without manual intervention.

0 Comments