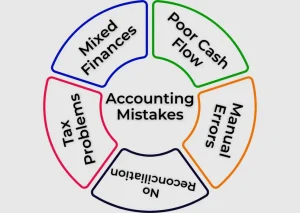

1. Mixing Personal and Business Finances

One of the biggest accounting mistakes at work is using the business account for personal expenses or using personal money to pay business bills.

Why It Matters

When you mix your personal money with your business money:

- Your accounting becomes messy.

- You can’t tell what the business truly made or lost.

- Tax time becomes a nightmare and you could face penalties.

How to Fix It

- Open a separate bank account for your business.

- Use only business cards for business expenses.

- Pay yourself a salary instead of taking money randomly.

Fixing this mistake will clear up your books and help you avoid one of the common accounting mistakes many owners make.

2. Poor Cash Flow Tracking

Many business owners assume that if their company shows a profit on paper, everything is fine. But even profitable businesses can run into trouble if they ignore cash flow, the money coming in and going out. Failing to monitor cash flow is one of the common accounting mistakes that can quietly hurt your business.

Why It’s a Big Deal

Cash flow is the lifeblood of any business. Without it, you could struggle to:

- Pay bills on time.

- Buy inventory or stock.

- Fund business growth and expansion.

Even businesses making a profit have failed simply because they ran out of cash. Ignoring cash flow is one of the accounting mistakes to avoid if you want to keep your business healthy.

How to Fix It

- Forecast your cash flow weekly or monthly to know how much money is coming in and going out.

- Follow up on unpaid invoices immediately to avoid delays.

- Keep a cash buffer—a little extra in the bank for emergencies or unexpected expenses.

By tracking cash flow consistently, you prevent accounting mistakes at work, ensure your bills are paid on time, and maintain a strong financial foundation for your business.

3. Manual Errors and Disconnected Records

If you or your team are entering numbers by hand or using unconnected systems like a separate CRM for customers and spreadsheets for finances, mistakes are almost inevitable. These kinds of errors are among the common accounting mistakes that can quietly disrupt your business operations.

Common Examples

- Typing the wrong number into expense records.

- Forgetting to record an invoice payment.

- Duplicating customer or transaction records across multiple systems.

Even small mistakes like these can lead to big problems: incorrect tax calculations, lost revenue, and confusing financial reports. Ignoring this is one of the accounting mistakes to avoid if you want your books to be reliable.

How to Fix It

- Use smart and reliable accounting software to centralize your records.

- Automate data entry wherever possible to reduce human error.

- Sync customer and transaction data across all systems to ensure consistency.

By addressing manual errors and disconnected records, you prevent accounting mistakes at work, maintain accurate financial records, and save valuable time for growing your business.

4. Not Reconciling Bank and Credit Accounts

At the end of every month, it’s important to check that your accounting records match your bank and credit card statements. This process is called reconciliation, and skipping it is one of the most common accounting mistakes to avoid.

Why This Mistake Is Costly

If you don’t reconcile your accounts:

- You may miss fraudulent or unauthorized transactions.

- Payments could be recorded twice or not recorded at all.

- Your financial reports won’t show the real picture of your business.

Ignoring this step is one of the common accounting mistakes that can grow into bigger problems over time.

How to Fix It

- Set a monthly habit of reconciling your books with your bank and credit card statements.

- Use accounting software that automates reconciliation to save time and reduce errors.

- Investigate any mismatched transactions immediately to avoid future problems.

Regular reconciliation prevents accounting mistakes at work, keeps your financial records accurate, and ensures you always know where your business stands.

5. Ignoring Tax Deadlines and Compliance

Taxes can be confusing for many business owners, and that’s exactly why mistakes happen. Missing deadlines, misunderstanding requirements, or filing incorrectly can cost your business money and create unnecessary stress. Ignoring taxes is one of the common accounting mistakes to avoid that can lead to serious problems.

Common Tax Mistakes

- Forgetting quarterly tax estimates.

- Not claiming all eligible deductions.

- Missing local or international tax requirements.

How to Fix It

- Keep a tax calendar with all deadlines clearly highlighted.

- Consult a tax professional at least once a year to stay compliant.

- Use accounting software that tracks deadlines and tax requirements automatically.

By staying proactive, you prevent accounting mistakes at work, avoid costly penalties, and make sure your business stays compliant with all tax rules.

Sum Up!

Here’s the truth: most business owners aren’t accountants, and that’s okay. What isn’t okay is letting accounting mistakes quietly eat into your profits and cause stress you don’t need.

The good news? These accounting mistakes are easy to fix. Separate your finances, automate systems, track cash flow, reconcile every month, and stay on top of taxes. Avoiding common accounting mistakes at work will make your financial picture clearer, your decisions smarter, and your business stronger.

Think of accounting as the foundation that keeps your business standing. With the right habits and tools, you’ll not only avoid costly mistakes; you’ll build a business that can grow with confidence.

0 Comments